As we say goodbye to April and head into May, the end of the financial year is suddenly right in front of us. But this year, 1 July 2026 brings more than just the usual tax time paperwork. It marks the official start of Payday Super.

With exactly two months to go, the team at Nova Business Services wants to make sure you are ready. Deputy Commissioner Emma Rosenzweig recently addressed some widespread misunderstandings about these new rules, and we want to break them down from a practical bookkeeping perspective.

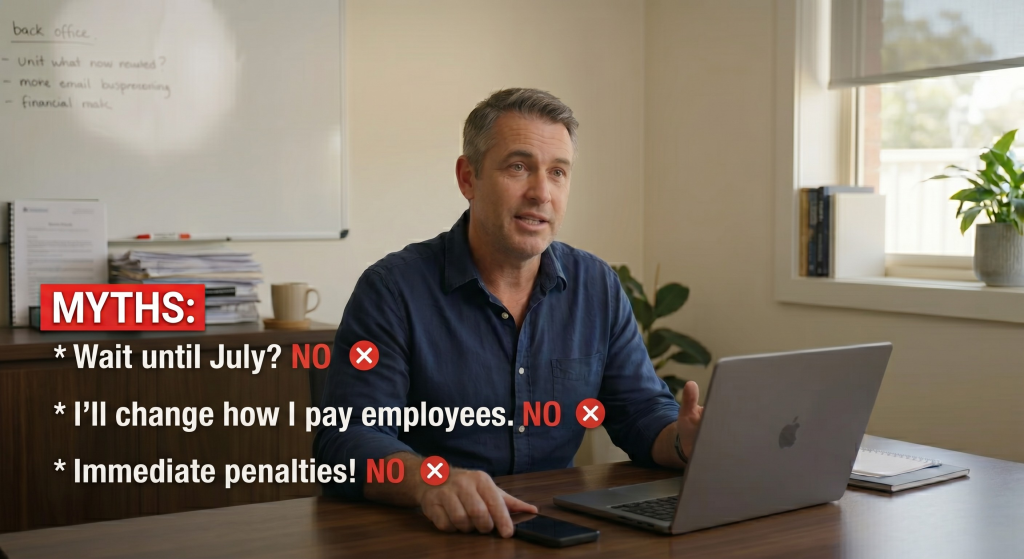

Here are the top three Payday Super myths and what you actually need to know to keep your business compliant.

Myth 1: There is nothing to do until 1 July 2026

It is incredibly dangerous to leave your preparations until the final week of June. While the legislation comes into effect on 1 July, your business needs to be ready well before then.

The biggest immediate change for many small businesses is the permanent closure of the ATOs Small Business Superannuation Clearing House, commonly known as the SBSCH. This portal shuts its digital doors for good on 1 July. The catch? There will be absolutely no read-only access once it closes. You must log in and download all your historical records right now to ensure you have them for your files.

Beyond saving your records, you also need to find and transition to a new superannuation provider or upgrade your current payroll software to handle the new frequency. More importantly, you need to forecast your cashflow. Moving from holding super funds for up to three months to paying them weekly or fortnightly is a massive adjustment to your working capital.

Myth 2: I can just change how often I pay my employees

Some employers think the easy fix is to simply alter their staff pay cycles to match their preferred superannuation schedule. Unfortunately, the law does not work like that.

Payday Super does not change how often you pay wages. Your pay frequency is legally bound by employment contracts, modern awards, or enterprise agreements. What changes is when the super must be paid out of your bank account.

From 1 July 2026, you must pay super each time you pay your staff. If you run a weekly payroll, you pay super weekly.

Crucially, the funds must be received by the employees super fund within seven business days after payday. Keep in mind that a payment only counts when the fund receives it, not when you hit submit in your payroll software. Because clearing houses can take a few days to process payments, waiting until day seven is incredibly risky. We strongly recommend processing the super payment on the actual payday to give yourself maximum breathing room.

Myth 3: I will be penalised straight away if something goes wrong

We know that structural changes to payroll can cause a lot of anxiety for employers who just want to do the right thing. The good news is that the ATO is taking a pragmatic approach to the transition.

If you make an honest mistake while adapting to the new Payday Super rules, you will not be the immediate target of compliance action, provided you take quick steps to fix the error. The ATO is focussing heavily on education and support during the first year, giving businesses a fair chance to adapt their internal systems.

How Nova Business Services can help

Navigating the end of the SBSCH, updating your software, and managing cashflow changes is a huge task to handle while running your day-to-day operations. Let the experts at Nova Business Services take the stress out of your EOFY. Reach out to our team today to ensure your transition to Payday Super is seamless, stress-free, and fully compliant.

Our team is here to support you and your business in many different ways, give us a call on 1800 668 225 or reply to this blog by clicking here to ask us any questions.